Oil Market Faces Supply Crunch Amid Hormuz Tt

Market faces pressure as oil inventories dwindle and risks linger.

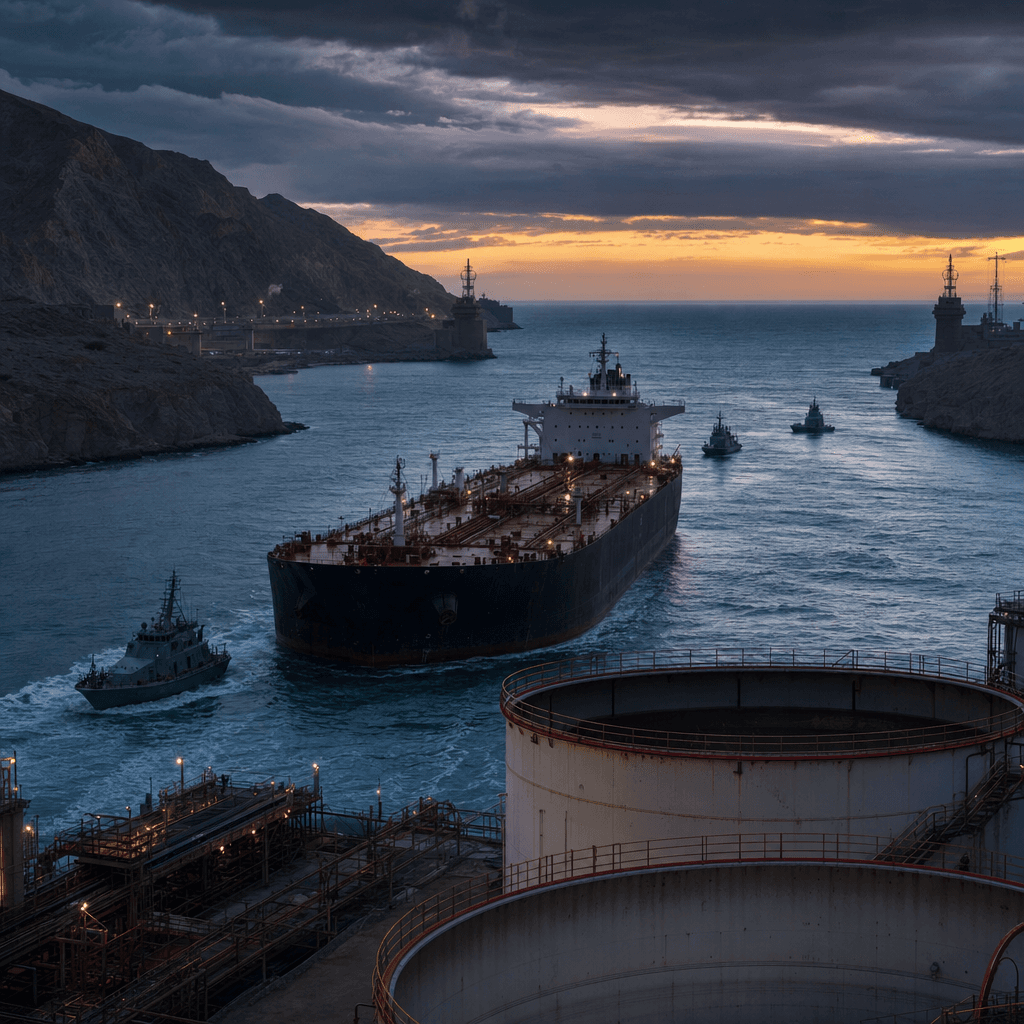

Model Diplomat3 min readGlobal

Oil Market Buffer Is Shrinking as Hormuz Risk Lingers

Inventory draws and a still-fragile Strait of Hormuz are giving the market only a short runway. The next few weeks will decide whether prices merely stay elevated or jump again.

The oil market is being held together by dwindling buffers, not by confidence that supply is fixed. Reuters says the market has about three months before tightening supplies start to bite in earnest, after global crude and fuel stocks fell at a pace of 5.27 million bpd in March and 8.62 million bpd in April, with draws expected to peak around 9 million bpd in May (Reuters). That is the real power dynamic now: whoever can keep the Strait of Hormuz constrained can keep the market under pressure, while everyone else is buying time.

The market is trading inventory depletion, not calm

Reuters’ core warning is that official forecasts assume the Strait reopens by late May and traffic resumes in June — a timetable the piece calls “highly optimistic” if peace efforts keep faltering (Reuters). The same report cites independent analyst Paul Horsnell projecting a steeper depletion path, with inventories falling by as much as 11.2 million bpd in June and some commercial stocks reaching minimum operating levels by August (

Reuters).

That matters because the market’s shock absorber is already being used up. Once inventories thin further, the response is not subtle: prices rise fast enough to force demand destruction. Reuters says Brent has already climbed about 50% since the war began to around $110 a barrel, and the article argues there is still room for more if the supply squeeze persists (Reuters). For

Global Politics, the lesson is simple: oil is now a geopolitical countdown clock, not just a commodity chart.

Who benefits from delay — and who pays

The short-term winners are the suppliers and intermediaries that can profit from scarcity. Saudi Arabia and other producers gain price support; Russia benefits from a market still willing to pay up for non-Gulf barrels, and Beijing’s large stockpile gives China one of the few external buffers if it chooses to draw down reserves (Reuters). By contrast, importers are left scrambling. In a separate report, Al Jazeera said the U.S. extended a 30-day sanctions waiver on Russian oil already loaded at sea to ease pressure on energy markets, but that the effect is limited because it covers only a narrow slice of supply (

Al Jazeera). The same piece said Russia was still exporting more crude and earning roughly $490 million a day from oil sales at around $100 a barrel (

Al Jazeera).

That is why Washington’s margin of maneuver is narrower than it looks. BBC reporting showed oil prices swinging on every hint that President Donald Trump might pause or resume strikes on Iran, and noted that higher energy costs were already pushing up borrowing costs and airline hedging costs (BBC News). In other words, signaling is now policy. For the

United States, every message on Iran, sanctions, or military restraint moves prices because the market believes the Strait may stay tight for weeks, not days.

What to watch next

The next decision point is whether transit through Hormuz improves by late May or remains constrained into June (Reuters). Watch the next EIA inventory figures, any fresh U.S. move on sanctions or strikes, and whether China begins drawing more aggressively on stockpiles (

Reuters,

Al Jazeera). If inventories keep falling at anything close to current rates, the market’s adjustment will no longer be gradual. It will be forced.

Discover more

Global Politics

US Seizes Iranian Ship, Tensions Surge

The US seizure of the Iranian ship Touska highlights a shift in control over the Strait of Hormuz, favoring Iran's strategic position.

Conflict & Security

West Africa Food Crisis: Three Shocks in 2026

Conflict, climate extremes, and the Strait of Hormuz closure drive a severe food crisis in West and Central Africa, with fertilizer prices surging 80% and millions displaced.

Conflict & Security

55M face hunger as three shocks hit Africa

Three shocks — Strait of Hormuz closure, Ebola Bundibugyo outbreak, and humanitarian funding collapse — converge on West and Central Africa during the 2026 planting season, threatening 55 million with acute food insecurity.

Economics

US Tariffs on Brazil: A Political Play

US imposes 25% tariff on Brazil but exempts 66% of exports, targeting manufactured goods ahead of Brazil's October election. Analysis of the political calculus, exemptions, and Brazil's response options.