Why India's Private Investment Is Slumping in 2026

Analyzing the factors behind India's investment decline

Model Diplomat3 min readAsia

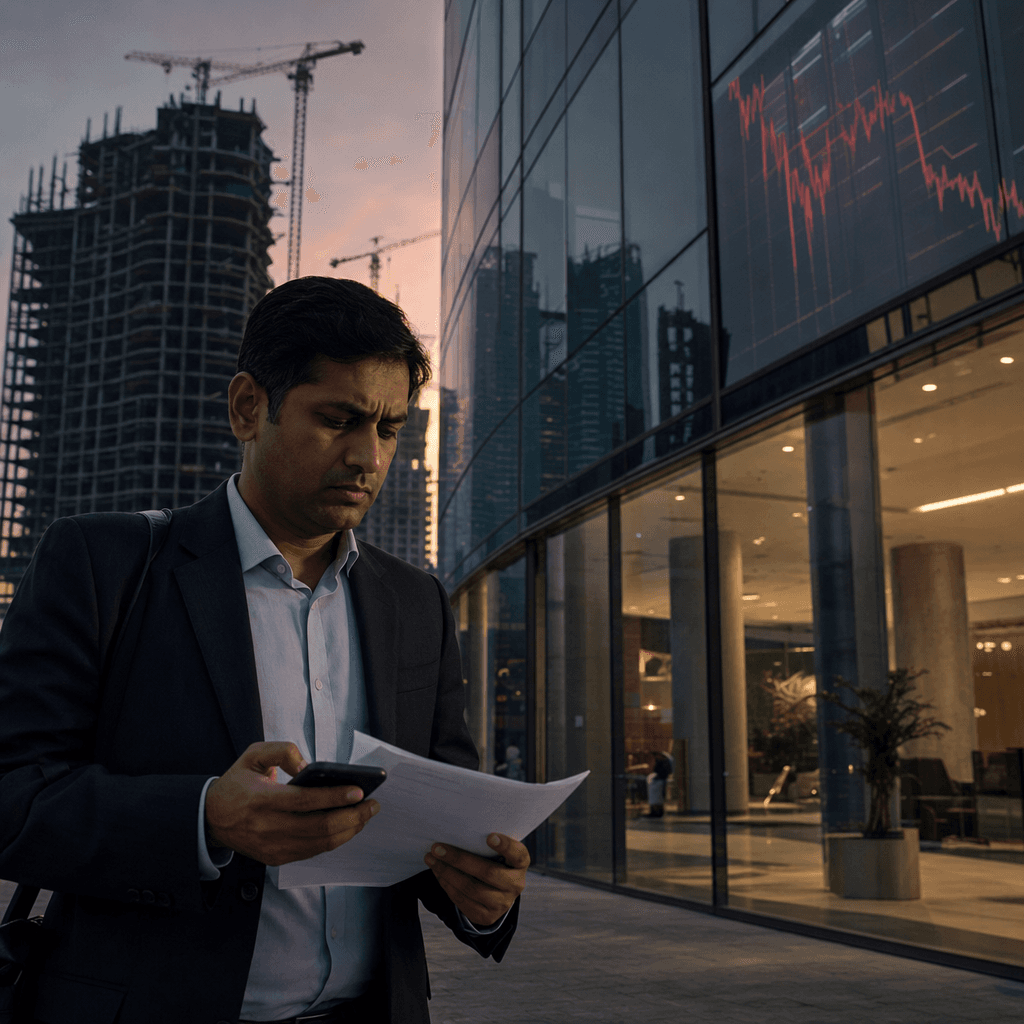

India’s Private Investment Slump Is a Confidence Test

Arvind Subramanian says investors are reading the rupee, not the reform list; the real problem is risk on the ground, not policy on paper.

Private capital in India is not sitting out because New Delhi has done nothing. It is sitting out because investors do not trust the operating environment. That is the core argument in Arvind Subramanian’s Indian Express column: private corporate investment peaked at 17 per cent of GDP in the early 2000s and is now roughly half that level, while the rupee’s weakness has exposed a deeper loss of confidence in India’s medium-term growth story.

The rupee is the warning light

Subramanian’s point is that the currency is not just a reaction to oil shocks or the Iran crisis. It is also a verdict on India’s growth prospects. He notes that the rupee was already the weakest performer among comparable emerging markets before the latest geopolitical shock, and that it fell by more than 20 per cent between 2022 and February 2026 despite heavy RBI intervention in spot and forward markets (Indian Express).

That matters because currency pressure raises the cost of imported capital goods, complicates hedging, and reinforces the sense that India is more vulnerable than its headline growth numbers suggest. For policymakers watching India, the message is blunt: a strong GDP print does not substitute for investor confidence when the currency keeps sliding.

Reform on paper has not fixed risk in practice

The government can fairly argue that it has already done a lot on the formal reform front. Subramanian lists cut-and-simplified GST, labour-law rationalisation, wider FDI liberalisation, two deregulation committees, and trade deals with the EU and the US as proof that the official “cost of doing business” agenda has moved (Indian Express). Yet the investment response has been weak.

That disconnect is where the politics bites. Subramanian argues that what scares investors is not just red tape, but arbitrariness: favoritism toward a few large groups, uneven treatment of BJP-ruled and opposition-ruled states, aggressive use of tax and enforcement powers, and weak federal decision-making (Indian Express). In other words, firms are not pricing only policy; they are pricing discretion.

A second reading, from The Hindu BusinessLine, points to a different but compatible constraint: demand. Its analysis says private firms do not invest if they cannot see future sales, and cites RBI data showing the private sector investment-to-GDP ratio falling from 28 per cent in 2011–12 to 21.1 per cent in 2022–23. Tax cuts and a bank clean-up did not trigger a boom because companies used the extra cash to deleverage rather than expand capacity (

The Hindu BusinessLine).

That is the important synthesis: India’s capex problem is not one thing. It is a mix of weak demand, tighter global financial conditions, and a domestic state that still looks unpredictable enough to scare off long-horizon investment.

What to watch next

The next test is whether the government changes the people and the tone around economic policy, as Subramanian urges, or keeps relying on the same faces and the same message discipline (Indian Express). If New Delhi keeps defending the currency while investors keep seeing discretion, not rule-bound governance, private investment will stay muted.

Watch the next fiscal and monetary signals: any fresh move on deregulation, any shift in personnel tied to economic management, and whether the RBI is forced to choose between currency defense and easier financial conditions. The real decision point is whether India tries to restore trust or just keep managing the optics.

Discover more

India

BJP's Misunderstanding of Women's Quota Needs

The BJP's linking of the Women Reservation Bill to delimitation risks delaying women's empowerment in India, misreading the aspirations of female voters.

Conflict & Security

West Africa Food Crisis: Three Shocks in 2026

Conflict, climate extremes, and the Strait of Hormuz closure drive a severe food crisis in West and Central Africa, with fertilizer prices surging 80% and millions displaced.

Conflict & Security

55M face hunger as three shocks hit Africa

Three shocks — Strait of Hormuz closure, Ebola Bundibugyo outbreak, and humanitarian funding collapse — converge on West and Central Africa during the 2026 planting season, threatening 55 million with acute food insecurity.

Economics

US Tariffs on Brazil: A Political Play

US imposes 25% tariff on Brazil but exempts 66% of exports, targeting manufactured goods ahead of Brazil's October election. Analysis of the political calculus, exemptions, and Brazil's response options.