India's 35-Country Minerals Web Explained

A strategic move to counter Chinese export shocks

Model Diplomat7 min readAsia

India's 35-Country Minerals Web: The Real Bet Is Against Beijing

India now runs critical-minerals cooperation with 35 countries — a diversification play built to survive the next Chinese export shock, not just this one.

New Delhi's disclosure on July 7, 2026 that it is now running critical-minerals cooperation with 35 partner countries is being presented as a supply-chain story. It is really a hedging story: after China's April 2025 rare-earth curbs cut magnet shipments to India by 58 percent and forced Bajaj Auto to halve production of its best-selling electric scooter, the Modi government has spent 18 months building a redundancy network — Quad money, Latin American lithium, French processing know-how, Australian midstream expertise — designed less to replace China than to make the next coercion attempt commercially and politically uneconomic for Beijing. That is the argument. The rest is engineering.

The shock that reset the doctrine

For years India treated critical-mineral dependency as a procurement problem. That framing collapsed on April 4, 2025, two days after President Donald Trump's "Liberation Day" tariffs, when China's Ministry of Commerce imposed export licences on seven medium and heavy rare-earth elements — samarium, gadolinium, terbium, dysprosium, lutetium, scandium and yttrium — plus rare-earth permanent magnets. According to Al Jazeera's reporting on the shortage, no magnet shipment reached India for months; Bajaj cut Chetak production to 24,000 units, and Maruti Suzuki flagged bottlenecks across its EV programme.

The Vivekananda International Foundation, citing Indian customs data, calculates that in fiscal 2024-25 India imported roughly 54,000 tonnes of rare-earth magnets, with 93 percent from China at an import bill of about ₹1,744 crore. When Beijing followed up on October 9, 2025 with MOFCOM Notice 61 — extending licensing extraterritorially to any product containing more than 0.1 percent Chinese-origin rare earths — the message was unambiguous. Supply was now a policy lever.

The Swedish Institute of International Affairs tracked what followed: global magnet exports fell 73 percent in May 2025 before selectively recovering, but exports of dysprosium oxide in raw form only resumed in August, and only to South Korea and Japan. India was, in effect, on a slower queue.

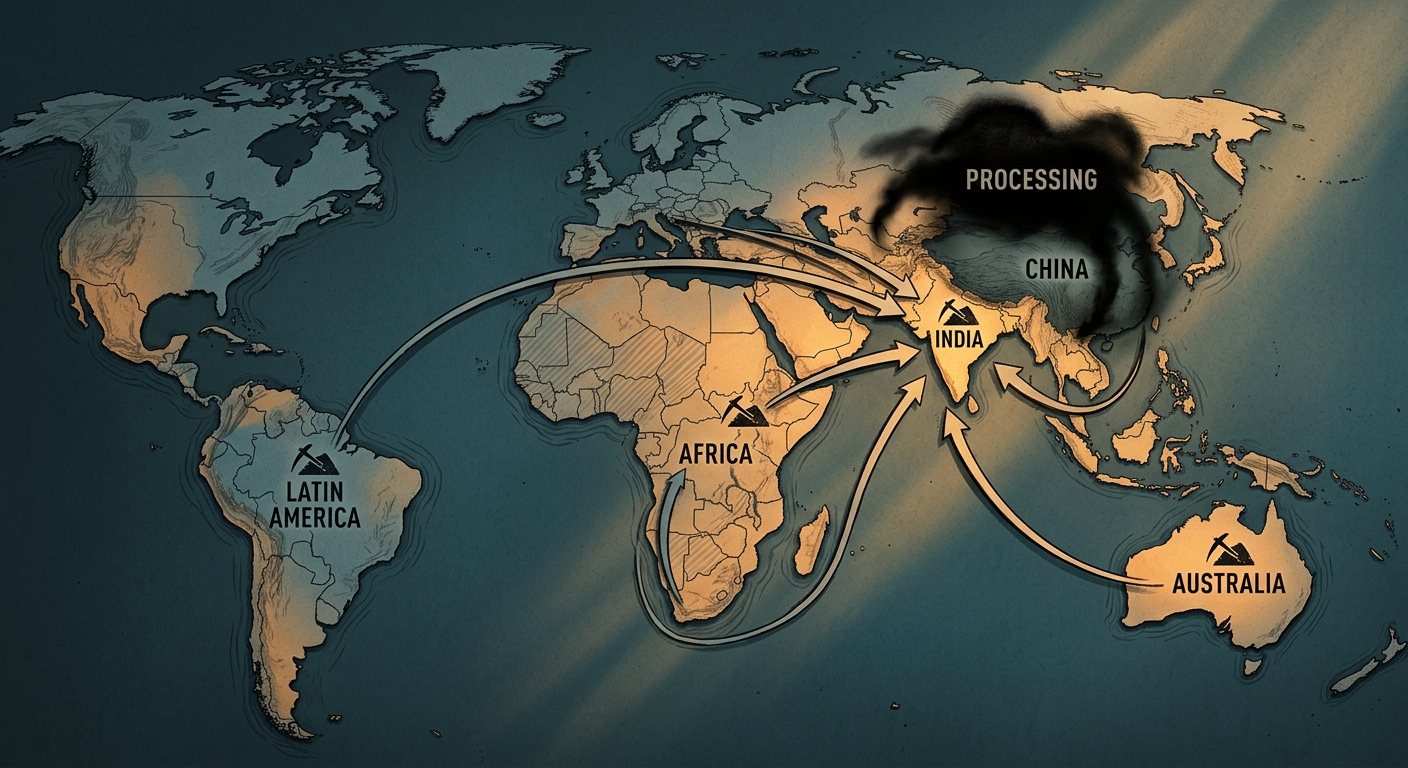

The 35-country architecture, decoded

The government's number sounds diplomatic. The instruments behind it are industrial. The Ministry of Mines' Press Information Bureau statement confirms that the Union Cabinet approved the National Critical Mineral Mission (NCMM) on January 29, 2025, with a ₹16,300 crore central outlay and roughly ₹18,000 crore in expected public-sector spending — a total of about $4 billion pointed at exploration, midstream processing parks, recycling and overseas asset acquisition, according to

India's parliamentary answer AU454 listing the 30 critical minerals in scope.

The NITI Aayog's Critical Mineral Assessment, released in February 2026, quantifies the stakes: under a Net Zero scenario, cumulative demand for critical energy-transition minerals hits about 169 million tonnes by 2050, with copper alone exceeding 20 Mt and graphite 14 Mt. Crucially, the report concedes that India's projected share of global demand — roughly 9 percent by 2050 — is "insufficient for price-setting power." Diplomacy is not a supplement to the domestic push; it is the mission.

The 35-country footprint fits into four concentric rings.

Ring one — Quad and the West. On May 26, 2026, External Affairs Minister S. Jaishankar and Secretary of State Marco Rubio signed a bilateral framework on "Securing Supply in the Mining and Processing of Critical Minerals and Rare Earths" in New Delhi, alongside a Quad Critical Minerals Initiative Framework. The Al Jazeera account of the deal puts the Quad mobilisation target at up to $20 billion in blended finance — loans, guarantees, subsidies and long-term offtake — spread across mining, processing and recycling in "like-minded" jurisdictions.

Ring two — the plurilateral clubs. India is now a founding member of the Forum on Resource Geostrategic Engagement (FORGE), which the Center for Strategic and International Studies reports succeeded the Minerals Security Partnership at the February 4, 2026 US Critical Minerals Ministerial, alongside 55 foreign delegations. India also holds a seat in Pax Silica, the December 2025 semiconductor-and-AI supply-chain forum with 13 signatories, which explicitly ties mineral access to compute and defence electronics.

Ring three — the producer states. Khanij Bidesh India Ltd (KABIL), the state joint venture spanning NALCO, Hindustan Copper and Mineral Exploration Corporation, holds five lithium brine blocks in Argentina's Catamarca province covering 15,703 hectares, and has bilateral MoUs with Australia's Critical Minerals Facilitation Office for lithium and cobalt. Observer Research Foundation reports that a Comprehensive Economic Partnership Agreement with Chile — the country with the world's largest lithium reserves — is under negotiation, and February 2026 deals with Brazil and France have added South American and European anchors, the

latter upgraded to a Special Global Strategic Partnership.

Ring four — the Global South. Ministry engagements now stretch to Zambia, Namibia, the Democratic Republic of Congo, Ghana and Bolivia — the ORF study on India–EU cooperation maps the overlap between India's outreach and the EU's 14 Strategic Partnerships since 2021, hinting at a coming convergence with Brussels' Global Gateway.

The non-obvious angle: this is a Franco-Brazilian bet as much as a Quad bet

The consensus reading — that India is quietly joining a US-led minerals bloc — misses what the terms actually say.

Analyst Chietigj Bajpaee and the ORF team have argued that India's Australia partnership is the only pact since 2024 that functions as a genuine industrial partnership, with technology transfer, joint R&D and downstream processing built in. Most others remain declarations. The February 2026 deals with France and Brazil matter because Brazilian President Lula explicitly announced a "new paradigm of mineral diplomacy" that April: extraction rights alone would no longer suffice; buyers must bring processing technology, downstream investment or offtake guarantees. France, under its 2026 Special Global Strategic Partnership, is offering separation and metallurgy know-how — the exact midstream stage where China holds a near-monopoly and where the Quad framework, so far, offers mostly capital.

The implication is inconvenient for Washington: India is diversifying processing partners in ways that make the US bilateral a ceiling, not a floor. When the CSIS analysis notes that the United States accounts for only 3.6 percent of global rare-earth consumption, Indian negotiators can read the leverage math too. That is why the 35-country framing — not the Quad framing — is the one Ministry of Mines officials keep repeating.

What Beijing sees, and what still doesn't work

China's April 2025 curbs did not cause India's diversification push; the National Critical Mineral Mission was already cleared in January. But the curbs did convert diversification from an EV-industry irritant into a national-security file. According to the

ETH Zürich Center for Security Studies, Chinese export controls are now calibrated in "days" rather than months, and price differentials between Chinese and international rare-earth markets have run as high as six-to-one — a coercion premium that changes the maths of any investment case.

Two constraints still bind. First, the midstream. India has 46 critical-mineral blocks auctioned across six tranches by early 2026, including seven with rare earths, and Budget 2026-27 established Dedicated Rare Earth Corridors in Odisha, Kerala, Andhra Pradesh and Tamil Nadu. Yet separation, refining and metallisation — the environmentally hazardous, capital-intensive middle of the value chain — remain undercapitalised. The

Rare Earth Permanent Magnet scheme, cleared in November 2025 with a ₹7,280 crore outlay for 6,000 tonnes of annual capacity across five units, is the first serious midstream instrument.

Second, timing. India's own NITI Aayog concedes that two-thirds of cumulative critical-mineral demand arrives after 2050. The Ministry of Mines' processing-park budget is ₹500 crore, with recycling at ₹1,500 crore, spread to 2030-31. That is thin against Chinese scale. As the Lee Kuan Yew School's

India–China critical minerals paper notes, Beijing accounts for roughly 70 percent of global rare-earth mining and over 90 percent of refining — a moat that a $4 billion mission and 35 MoUs will not close in this decade.

Diplomat View

The 35-country partnership network will not make India mineral-independent by 2030 — and it does not need to. Its job is narrower and more political: to raise the price Beijing pays every time it reaches for the export-licence lever. If, by end-2027, India has at least one commercial-scale rare-earth separation line operating under the REPM scheme, plus a Chile CEPA signed and KABIL's Argentine blocks delivering first battery-grade lithium, the doctrine will have worked. If the midstream slips — if processing parks remain PowerPoint by 2028, or if the India–US framework produces investment on paper but no offtake for Indian refiners — this becomes another minilateral photo-op stack, and the leverage stays in Beijing's hands. The falsifiable call: watch the Ministry of Mines' first "mineral processing park" allocation and the India–Chile CEPA negotiating text. Those two documents, more than any Quad statement, will tell you whether the 35-country map is real infrastructure or diplomatic theatre. This is the sharper edge of India's energy-security recalibration — and the reason it belongs in the same file as the Indo-Pacific security debate, not the trade one.

What to watch next

- September–November 2026: First implementing arrangements under the May 26 India–US and Quad Critical Minerals frameworks — capital commitments and named projects, or drift.

- Q4 2026: Award of Rare Earth Permanent Magnet manufacturing units under the ₹7,280 crore scheme; five sites are on offer, and the winners will determine whether India can move from mining to magnets at commercial scale.

- Early 2027: Expected conclusion of the India–Chile Comprehensive Economic Partnership Agreement, the largest producer-state deal in New Delhi's pipeline.

- 2027 FORGE ministerial: Whether preferential trading arrangements and price floors — floated at the February 2026 Washington meeting — materialise, and whether India signs.

The Bottom Line

India's 35-country critical-minerals web is not a bid for autarky; it is a strategy to make Chinese coercion expensive enough to deter. The wager rides on whether New Delhi can turn Franco-Brazilian and Australian midstream know-how — not Quad capital — into commercial-scale processing at home by 2028. If it can, the next April 2025 will look like a nuisance; if it cannot, the 35-country map is just a longer list of MoUs.

Discover more

US Politics

House Ethics Committee Pushes Sexual Miscond.

The House Ethics Committee has shifted responsibility for sexual harassment settlement records to the Office of Congressional Workplace Rights, complicating disclosure efforts.

US Politics

SNAP Food Assistance Faces Legal Challenges

In 2026, SNAP faces stricter eligibility rules and mounting legal challenges, threatening food assistance for the millions of Americans who rely on the program.

International Relations

Pakistan's Key Role in US-Israel-Iran Meddle

Pakistan is seeking to mediate the US-Israel-Iran conflict, balancing high-stakes diplomacy against severe economic pressures and steep regional challenges.

Global

Zimbabwe's 2030 Gambit: Mnangagwa's Rule

Zimbabwe's Constitutional Amendment No. 3 ends direct presidential elections, extending Mnangagwa's rule to 2030 and raising concerns over democratic integrity.