Bretton Woods Made the Dollar

Exploring the legacy of Bretton Woods on global finance

Model Diplomat3 min readGlobal

Bretton Woods Made the Dollar — and Still Defends It

The 1944 Bretton Woods bargain was a power settlement, not a technical fix: it put Washington at the center of global money, and that legacy still shapes leverage today.

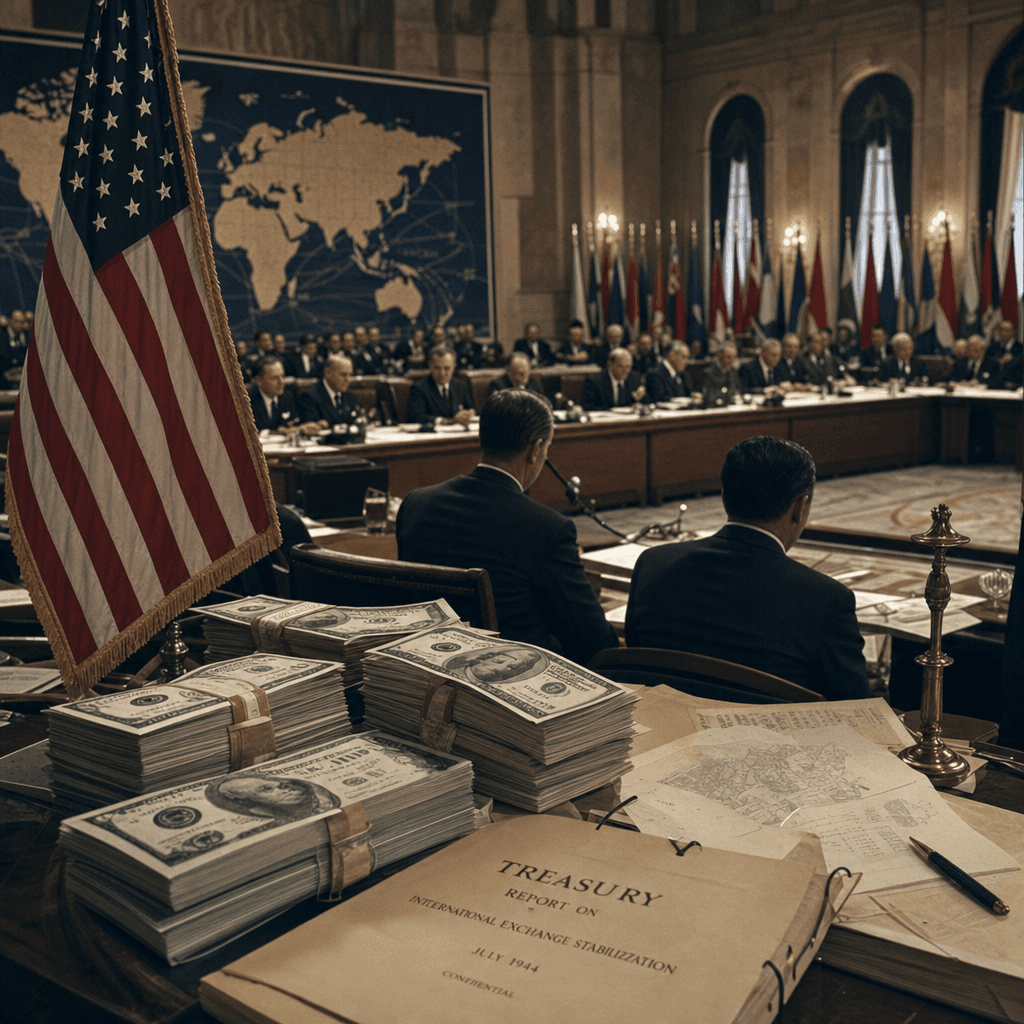

The Financial Times’ account of Bretton Woods is a reminder that the dollar’s rise was not an accident of markets; it was an American-designed order built in the last year of World War II, when the U.S. had the gold, the industrial capacity, and the bargaining power to dictate the terms (Financial Times). The agreement emerged from three weeks of talks at a remote New Hampshire hotel with 730 delegates from 44 countries, and it produced the IMF, the World Bank, and a system that tied other currencies to the dollar, with the dollar itself convertible into gold (

Financial Times;

FT transcript).

The real prize was leverage

That institutional design mattered because it gave the United States more than prestige. It gave Washington the ability to finance deficits in its own currency, shape crisis lending through the IMF, and anchor trade in dollars rather than any rival unit (FT transcript). Britain’s John Maynard Keynes wanted a more symmetric system with a global clearing union and a new reserve asset; U.S. negotiator Harry Dexter White pushed a dollar-centered architecture, and White’s version won (

Financial Times;

FT transcript). For today’s policymakers, the lesson is simple: reserve-currency status is not just about liquidity; it is about institutional control.

That is why the historical debate still echoes in Global Politics and in the

United States profile: the dollar system is both an economic convenience and a geopolitical instrument.

The system survived its own collapse

The original Bretton Woods exchange-rate regime lasted only until 1971, when the U.S. closed the gold window, but its institutions and habits outlived the peg (GEOPOL). That durability is the point. Even as the formal system broke, the dollar stayed central because there was no clean substitute and because global markets kept recycling into U.S. assets (

GEOPOL). Brookings argues that, despite recent volatility, reserve managers have not meaningfully fled the dollar because the hurdle to replacing it remains high and no credible alternative has emerged (

Brookings).

But the order is less uncontested than it looks. CFR notes that sanctions pressure and U.S. financial coercion are pushing some actors to build workarounds, including China-linked payment channels and non-dollar settlement for sensitive trade (Council on Foreign Relations). That does not dethrone the dollar. It does, however, tell rivals that escaping the system is possible at the margins — especially when Washington uses the system too aggressively.

What to watch next

The next test is not whether the dollar disappears. It is whether more trade, reserves, and sanctions-sensitive flows move into small-currency or China-linked alternatives at the margin, eroding U.S. leverage without producing a single replacement (Brookings;

Council on Foreign Relations). Watch the IMF, the Bank for International Settlements, and the next sanctions episode: that is where the power balance will show up first, not in speeches about “de-dollarization.”

Discover more

International Relations

Bretton Woods: The Dollar's Lasting Dominance

The Bretton Woods agreement established the dollar's central role in global finance, and its legacy still shapes the IMF, monetary policy, and world markets.

International Relations

Bretton Woods: Dollar's Power Dynamics Revea

The Bretton Woods agreement cemented the US dollar's dominance in global finance while exposing systemic weaknesses that still shape the IMF and worldwide

Global

Zimbabwe's 2030 Gambit: Mnangagwa's Rule

Zimbabwe's Constitutional Amendment No. 3 ends direct presidential elections, extending Mnangagwa's rule to 2030 and raising concerns over democratic integrity.

Global

Xi's September White House Visit Tests Truce

Trump to host Xi on September 24, 2026, to discuss a new phase in US-China trade relations amid ongoing tensions over Taiwan and technology.